Delve into the world of small business health insurance providers as we uncover the top players, key features, and pricing structures. Get ready for an informative journey filled with valuable insights and comparisons.

Overview of Small Business Health Insurance Providers

When it comes to choosing a health insurance provider for your small business, it's important to consider the top options available in the market. Here are some of the top small business health insurance providers and the key features they offer:

List of Top Small Business Health Insurance Providers:

- Aetna: A well-known provider offering a wide range of plans and coverage options.

- Blue Cross Blue Shield: Known for its extensive network of healthcare providers and customizable plans.

- Cigna: Offers comprehensive coverage and wellness programs for employees.

- UnitedHealthcare: Provides a variety of plan options and additional resources for employers.

Key Features and Benefits:

- Customizable plans to fit the needs of your business and employees.

- Access to a network of healthcare providers for quality care.

- Wellness programs to promote employee health and reduce healthcare costs.

- Dedicated customer support for any insurance-related queries or issues.

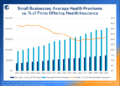

Comparison of Pricing Structures:

| Provider | Basic Plan Cost | Additional Coverage Options |

|---|---|---|

| Aetna | $300/month | Dental, Vision, Mental Health |

| Blue Cross Blue Shield | $350/month | Pregnancy, Prescription Drugs, Chiropractic Care |

| Cigna | $320/month | Wellness Programs, Telemedicine, Employee Assistance |

| UnitedHealthcare | $310/month | Preventive Care, Chronic Condition Management, Virtual Visits |

Coverage Options and Plans

When it comes to small business health insurance providers, there are various coverage options available to meet the diverse needs of businesses. Different providers offer different types of health insurance plans, each with its own set of benefits, coverage limits, and exclusions.

It's important for small business owners to understand these options to choose the best plan for their employees.

Types of Health Insurance Plans

- Health Maintenance Organization (HMO): These plans require employees to select a primary care physician and get referrals for specialists. They generally have lower out-of-pocket costs but limited provider networks.

- Preferred Provider Organization (PPO): PPO plans offer more flexibility in choosing healthcare providers without referrals. However, they often come with higher premiums and out-of-pocket costs.

- Exclusive Provider Organization (EPO): EPO plans only cover services from in-network providers, except in emergencies. They may have lower premiums compared to PPO plans.

- Point of Service (POS): POS plans combine features of HMO and PPO plans, allowing employees to choose in-network or out-of-network providers. Referrals are usually required for specialists.

Coverage Limits and Exclusions

- Many health insurance plans have coverage limits, such as annual or lifetime maximums on benefits. It's essential for small business owners to understand these limits to ensure adequate coverage for their employees.

- Exclusions are specific services or treatments that are not covered by the insurance plan. Common exclusions may include cosmetic procedures, elective surgeries, or alternative therapies.

- Some plans may also have waiting periods for certain services, pre-existing condition limitations, or restrictions on coverage for specific treatments or medications.

Network of Healthcare Providers

When choosing a small business health insurance provider, it is essential to consider the network of healthcare providers associated with each option. This network determines which doctors, hospitals, and other medical facilities are covered under the insurance plan.

Comparison of Networks

- Provider A: Provider A has a large network of healthcare providers spread across multiple states, giving businesses and employees access to a wide range of medical professionals and facilities.

- Provider B: On the other hand, Provider B has a smaller network that may be limited to specific regions, potentially restricting the choice of healthcare providers for small businesses.

- Provider C: Provider C offers a medium-sized network that falls between the other two options, providing a balance between accessibility and choice.

Impact on Choice

- The size and scope of the network of healthcare providers can significantly impact the choice of a small business health insurance provider. A larger network may offer more options and flexibility for employees to choose their preferred healthcare providers.

- However, a smaller network could result in limited choices and potentially longer wait times for appointments, affecting employee satisfaction and overall healthcare experience.

- Businesses should consider the specific needs of their employees, such as preferred doctors or medical facilities, when selecting an insurance provider based on network coverage.

Customer Service and Support

Customer service is a crucial aspect to consider when choosing a health insurance provider for your small business. It can greatly impact the overall experience for both you as the business owner and your employees.

Customer Support Channels

- Phone Support: Most insurance providers offer a dedicated phone line for customer inquiries and support. This allows you to speak directly to a representative and get immediate assistance.

- Email Support: Another common channel is email support, where you can send in your queries or concerns and receive a written response from the customer service team.

- Online Chat: Some insurance providers have live chat support on their websites, providing real-time assistance to customers looking for quick answers.

Responsiveness and Effectiveness

When evaluating customer service, it's essential to consider the responsiveness and effectiveness of the support team in handling queries and issues. Here are some factors to keep in mind:

- Timely Responses: A good insurance provider should respond to customer inquiries and issues promptly, ensuring that your concerns are addressed in a timely manner.

- Knowledgeable Staff: Customer support representatives should be well-trained and equipped to provide accurate and helpful information to resolve any issues.

- Problem Resolution: The effectiveness of customer support can be gauged by how well they handle and resolve issues faced by small business owners and their employees.

Online Tools and Resources

Small business health insurance providers offer a variety of online tools and resources to assist business owners in managing their insurance policies effectively.

Comparison of Online Portals

- Providers offer user-friendly online portals that allow small business owners to easily view and manage their insurance policies.

- Features such as policy details, claims information, and billing statements are readily accessible through these portals.

- Some portals even offer mobile apps for added convenience, allowing users to access their information on the go.

Facilitation of Insurance Management

- Online tools streamline the insurance management process for small business owners by providing a centralized platform for all policy-related activities.

- Business owners can quickly make updates to employee information, add or remove coverage, and track claims status through these portals.

- The availability of online resources reduces the need for manual paperwork and phone calls, saving time and improving efficiency.

Customization and Flexibility

When it comes to small business health insurance providers, customization and flexibility are key factors that can help businesses tailor their plans to meet their specific needs.

Level of Customization

Different insurance providers offer varying levels of customization for small businesses. Some providers allow businesses to mix and match coverage options to create a plan that suits their unique needs. Others may offer pre-packaged plans with limited customization options.

- Some insurance providers offer a range of deductible options, allowing businesses to choose a deductible that fits their budget.

- Businesses may have the flexibility to add or remove coverage elements such as vision or dental insurance based on their employee needs.

- Providers may also offer different co-payment and coinsurance options, giving businesses the flexibility to choose a plan that works best for their employees.

Tailoring Health Insurance Plans

Small businesses have the opportunity to tailor their health insurance plans to suit their specific needs by considering the following factors:

- Assessing the healthcare needs of their employees and choosing coverage options accordingly.

- Considering the budget constraints of the business and selecting a plan that provides adequate coverage at an affordable price.

- Reviewing the network of healthcare providers to ensure employees have access to quality care.

Last Point

In conclusion, exploring the realm of small business health insurance providers reveals a landscape rich in options and considerations. Make informed decisions for your business's healthcare needs with the knowledge gained from this guide.

Expert Answers

What are the top small business health insurance providers?

The top providers include Aetna, UnitedHealthcare, Cigna, Humana, and Kaiser Permanente.

How can small businesses customize their health insurance plans?

Providers offer varying levels of customization, allowing businesses to adjust coverage elements to suit their specific needs.

What impact does network coverage have on choosing a health insurance provider?

Network coverage affects access to healthcare providers and services, influencing the overall value of the insurance plan.

Are there online tools provided by these insurance providers?

Yes, providers offer online portals for managing policies, facilitating ease of access and policy management for small business owners.

How do customer service levels vary among different insurance providers?

Customer service quality can vary, with some providers offering multiple support channels and responsive assistance, while others may have limitations.

{kind=link}